The BBC ran a good article pointing out that it will soon be rent-freedom day, which is analogous to the Adam Smith Institute's tax-freedom day.

So one-half of their earnings go in tax (stealth or otherwise) and one-third goes in rent. That means the average working tenant's disposable income after tax and housing costs is one-sixth of their earnings!

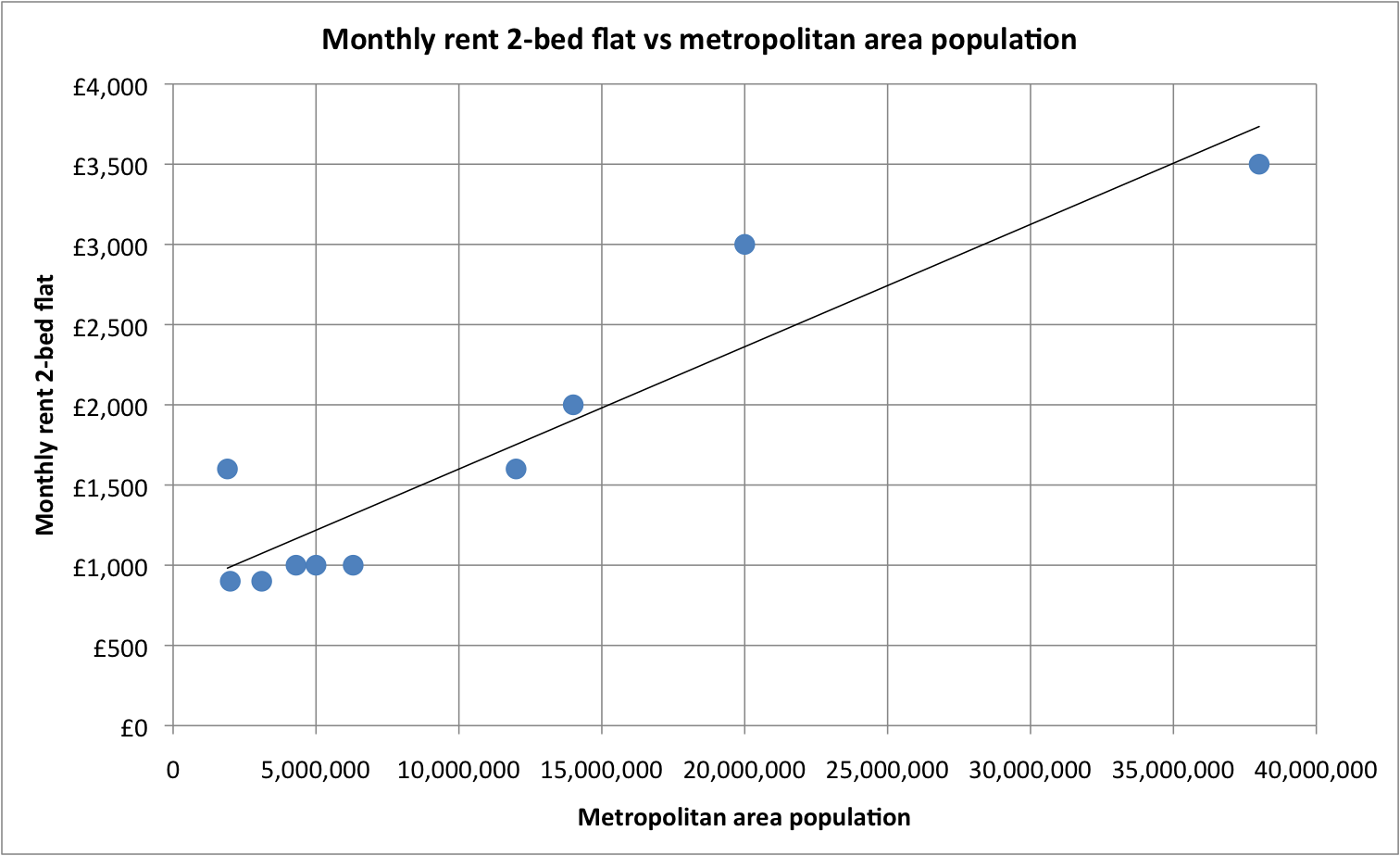

What caught my eye was this graphic further down the article:

Those rents are fairly proportional to the size of the population of those cities and their metropolitan/surrounding areas, co-efficient of correlation 0.93 (says Excel):

What's the relevance of this, you may ask (except for BenJamin' who put me onto this in the first place).

The point is that larger populations push up rents (agglomeration effects). If you build more homes in large cities, the simplistic supply-demand assumption is quite simply incorrect (unless you prevent any immigration into the city, which is impossible). Build more homes = more people = even higher rents. Rinse and repeat.

Sources:

https://en.wikipedia.org/wiki/Tokyo

https://en.wikipedia.org/wiki/New_York_metropolitan_area

https://en.wikipedia.org/wiki/London

https://en.wikipedia.org/wiki/Paris_metropolitan_area

https://en.wikipedia.org/wiki/Greater_Dublin_Area

https://en.wikipedia.org/wiki/Demographics_of_Berlin

https://en.wikipedia.org/wiki/Rome

https://en.wikipedia.org/wiki/Madrid_metropolitan_area

http://worldpopulationreview.com/world-cities/brussels-population/

https://en.wikipedia.org/wiki/Warsaw_metropolitan_area

Monday, 30 April 2018

World cities - rents vs metropolitan area population

Sunday, 29 April 2018

Killer Arguments Against LVT, Not (439)

Bayard posted this a few weeks ago. He didn't present it as an argument against LVT but said it was not necessarily an argument for, but nonetheless, it is clearly incorrect:

The argument for LVT: "... the private collection of rent is not only economically imprudent because it periodically destroys the economy, it is wrong!"

Leaving aside the periodic destruction of the economy, I don't think that it is a valid argument for LVT that it will be an instrument of social justice. This idea has quite some traction, especially amongst the ranks of the class warriors and ties into the populist landlord-bashing cause of enduring appeal.

His argument seems to be that rents will just increase, leaving tenants and first time buyers no better off, i.e. no improvement in 'affordabiity', however defined.

There are three overlapping concepts here - "social justice", "affordability" and "income/wealth equality". To simplify the way I understand them:

"Social justice" means everybody gets an equal share of whatever it is we are talking about. So, for example, in a democracy, every adult gets one vote 'for free', this has nothing to do with income or wealth equality.

"Affordability" means maximising people's incomes after housing costs, whether it changes income/wealth equality or not.

The best measure of "income/wealth equality" is net incomes after tax and housing costs. Landlords are at the top of the heap, their income IS other people's housing costs; owner-occupiers and council tenants break even; and private tenants or recent first time buyers are at the bottom of the heap.

Even if a landlord, an owner-occupier, a council tenant and a private tenant/recent first-time buyer have the same earned income from an actual job or productive business, their net of housing costs income varies enormously.

Let's look at UK housing policy in the 20th century to illustrate.

Back in 1900 or so, only a few people were owner-occupiers and everybody else rented from a few private landlords. This clearly leads to massive wealth/income inequality, as the tenants were left over with the bare minimum and the few landlords lived the life of Riley.

Fearful of a Socialist revolution, councils started building social housing, which was much cheaper and/or better than what private landlords were prepared to offer. Even more fearful after World War I, the UK government introduced rent controls.

The Tories noticed that council tenants are more likely to vote Labour and owner-occupiers more likely to vote Tory, so their counter-play was to encourage new construction and ensure that prices remained affordable by capping mortgages (and hence house prices).

Private landlords were squeezed out of the market - undercut by council housing and prevented from out-bidding private purchasers of new housing by rent controls and high taxation of rental income.

By 1980 or so, 70% of households were owner-occupiers; 30% were council tenants and only 10% rented privately. Between them, Labour and Tories did a great job.

In the UK, council rents were below market rents. The land rent element, which would have been used to pay a Citizen's Dividend was not collected in the first place. From a council tenant's point of view, it comes to much the same thing whether he pays £80 a week for the bricks and mortar cost (below market rent), or pays full market rent £200 a week (to include the land/location element) and his household gets a Citizen's Dividend of £120 a week. That £80 a week is clearly very affordable for all but the poorest couple of percent. The rest of your income is yours to spend on nice stuff!

Apart from a few years paying off the mortgage (capped at just above new-build costs - so little land rent element), owner-occupiers were benefitting from location rents without having to actually pay for them; again, that rent/mortgage saving is like a Citizen's Dividend. Once you have paid off the small mortgage, the rest of your income is yours to spend on nice stuff!

Therefore, with LVT in place, whether it is used to reduce other taxes or paid out as a Citizen's Dividend, we would all effectively be somewhere in between council tenants and owner-occupiers; the net housing cost is reduced to little more than the bricks and mortar cost of housing (just like it is for council tenants and owner-occupiers with a small or no mortgage).

That's "social justice" (everybody gets his share or land rent without having to pay for it), "affordability" (council rents and mortgages minus Citizen's Dividend are a smaller proportion of earned income subject to lower taxes ) and more "income/wealth equality" (as between landlord class and everybody else, or between Baby Boomers and Millennials, or between people in different parts of the country).

All with the bonus that there is a continual free market allocation (price rationing) of the best and worst sites (you want more, you pay more into the pot to be shared between everybody else).

There is no point arguing that 'landlords will put up the rent'. If they do, then LVT receipts will go up accordingly, and taxes on earnings and output will go down and/or Citizen's Dividend will go up, leaving most households unaffected in net terms.

Saturday, 28 April 2018

Outbreak of common sense in Islington

Opinions are divided on the topic of 'affordable housing' quotas*, and I am pretty indifferent either way, but rules are rules.

The scam in question goes like this, based on a real life example that Peter S helped me piece together:

1. Developer bought some land in London pre-2008. He planned to build 100 units, 30 affordable units were to be sold at break even and he hoped to make £100,000 profit (i.e. selling price minus construction costs but ignoring the land price) on each of the other seventy unaffordable units = £7 million profit. The amount he paid for the land was a large chunk of this £7 million, call it £5 million, leaving £2 million normal builder's profit.

2. In 2009, selling prices had fallen. The developer managed to get the affordable quota reduced to zero by submitting a new viability assessment...

3. The developer's logic was this: the profit per unaffordable unit has fallen from £100,000 to £70,000, so to make my normal builder's profit and recover the £5 million I paid for the land, I have to be allowed to sell all 100 units for the new (lower) unaffordable price.

4. The council gave in, scrapped the affordable quota and told him to get on with it.

5. The developer cheerfully did nothing for a few years until prices had recovered back to pre-2008 levels. So the potential profit was now 100 units x £100,000 = £10 million; £3 million more than he had originally hoped for.

6. The council did not re-impose the affordable quota, even though logic says they should have done.

7. That developer then sold the land to another developer for nearly £3 million more than he had paid for it pre-2008 (to reflect the additional £3 million profit which the next developer can make).

8. Clearly, if the council now tries to re-impose the affordable quota, the second developer can submit his own viability assessment, and say that if he is not allowed to sell all 100 units for the unaffordable price, he will be pushed into losses, bearing in mind the £8 million he paid for the land.

9. As we can see, viability assessments and the price paid for land are a circular argument.

The Planning Inspectorate has finally decided that overpaying for land (or falling prices) are simply not an excuse to wriggle out of the affordable quotas any more.

Islington’s housing boss Cllr Diarmaid Ward said the decision would help stop developers “manipulating” the viability process.

He said: “Islington, like all boroughs in London, faces a significant shortage of affordable homes. A viability process in planning that allows developers to rely on a flawed approach to market value that delivers little or no affordable housing makes this problem worse, and means developers are not making a fair contribution to the community.

“The decision sends a strong signal that developers need to take into account planning policy requirements when bidding for land, and that they cannot overbid and seek to recover this money later through lower levels of affordable housing.”

------------------------------

* On a very small scale, I don't think it has much impact and normal supply-demand rules apply, whereby selling prices are dictated by the incomes of potential purchasers. A developer would normally sell all finished units for the same price - based on the average incomes of all purchasers (price differentiation is nigh impossible).

If some units have to be sold for a lower price (and a much lower profit), then that takes the lower-earners out of the market. The average income of the remaining purchasers is therefore higher, so the unaffordable units can be sold for a higher price and the overall average selling price is not wildly different.

It is however a beggar-my-neighbour situation. An individual developer is always better off he can wangle a lower affordable quota that other developers in the same geographical area. Taking all developers in that area together, it doesn't make much difference.

Friday, 27 April 2018

The Trumps and Macrons arranged in order of age

Facebook profits - $2.27 per active user

From The Independent:

Facebook profits soared 63 per cent to $5bn (£3.6bn) in the first three months of the year despite the company being engulfed in a data privacy scandal that has angered millions of users.

from Statista:

As of the fourth quarter of 2017, Facebook had 2.2 billion monthly active users.

Reader's Letter Of The Day

From The Metro:

Fatting up Damian was unacceptable

If director Ricky Tollman needed an actor to play overweight, scandal-hit former Toronto mayor Rob Ford in 'Run This Town', why didn't he cast an overweight one?

'Fatting up' the slim Damian Lewis, however successful, is no more acceptable than having a white actor black up to play Othello.

Geoff, Stockport

I just can't decide if he's being serious or satirical...

Thursday, 26 April 2018

Summary of a conversation I had with a journalist today about Land Value Tax.

A journalist (who shall remain nameless as I do not disclose my sources:-) rang me this morning to chat about Land Value Tax, so we met at lunchtime to go through an implementation proposal I had drafted, I can't find the spreadsheet we were looking at, but apparently it's on the Labour Land Campaign website somewhere.

To summarise, including the stuff I didn't say, but wish I had...

1. I am a simplification campaigner as much as a pro-LVT campaigner. Even the worst taxes or subsidies can be made a bit less bad if they are at least simple and netted off as far as possible - there is no point subsidising something and taxing that same thing. Either pay a small net subsidy (and don't tax it at all) or tax it at a lower rate (and scrap the subsidy). At least that is the honest thing to do.

2. LVT is clearly the least bad kind of tax, compared to horrors like National Insurance or Value Added Tax. Endless articles have been written about why LVT is good and other taxes are bad, and either you understand them or you don't. I can explain stuff, but I can't make people understand stuff which they don't want to understand. (I can hear and I understand how sound waves and the inner ear works, but I can't give deaf people their hearing back).

3. The only real 'problem' with Land Value Tax is political. In the UK, we have a weird slavish worship of house prices. The last half century has shown, if house prices are rising, the party in government will be re-elected; if they are falling, the opposition party will win. So the politicians, of whatever party, don't like to utter the words "Land Value Tax" because - it is widely believed - this tax would push down house prices.

4. The UK already has a dozen fairly minor taxes (which between them only raise about one-tenth of total taxes) on housing, land values and private wealth generally. If we - in the interests of simplification if nothing else - replaced all these with a flat-rate LVT, there would be little impact on house prices and most households would pay the same total amount of tax over a lifetime as they do now. So this should be politically acceptable, assuming a rational electorate. (Business Rates just needs a few tweaks and it's LVT, that's a minor issue).

5. Annual revenues from the specific taxes in that spreadsheet (figures two or three years out of date) were as follows:

Council Tax - England - £24 bn

Council Tax - Scotland - £2 bn

Council Tax - Wales - £1 bn

Domestic Rates - N Ireland - £1 bn

Less Council Tax benefit, rebates etc - £(5 bn)

Stamp Duty Land Tax on housing - £8 bn

Capital Gains Tax - £6 bn

Inheritance Tax - £4 bn

TV licence - £4 bn

Stamp Duty on shares - £3 bn

Insurance Premium Tax - £3 bn

Let's call it £50 bn per annum, all in.

(Maybe we could scrap Housing Benefit for private landlords and exempt private landlords from income tax as a quid pro quo, in which case, the required revenues are only £45 bn. And scrap Help To Sell Buy, in which case, required revenues are only £44 bn and so on.)

6. The purists are quite correct to say that LVT should be based on site premiums i.e. the potential rental value of land and buildings, minus the cost/value of the actual physical building (referred to as the "Site-only rental value assuming optimum permitted use"). For a low level LVT, it is quite sufficient to base it on potential selling prices. So the purists say that £50 bn can be raised with a tax calculated as 25% of site premiums. The not-so-purists say that £50 bn can be raised with a tax calculated as 0.7% of potential selling prices. Comes to much the same thing.

Either way, there has to be some system of valuations, so I explained how we can adapt the Council Tax system very easily to get 80% - 90% of the way there. Is this the best way of doing it? For an expert valuer, clearly not. For administrative simplicity, I think yes, until somebody can think of something simpler and better, then I'll support that instead.

7. To summarise this summary: the UK already has LVT!! It is just diced and sliced and heavily disguised - the little people pay Council Tax and the TV licence fee every year; buyers/sellers pay Stamp Duty Land Tax; landlords and second home owners pay Capital Gains Tax when they sell; the really wealthy pay Inheritance Tax when they die; super wealthy foreigners pay the Annual Tax on Enveloped Dwellings etc. Each of these taxes is a minor tax, raises relatively little revenue and is fiddly and bad tax in itself, with all sorts of cliff-edges and unintended consequences.

If you replace them all with LVT, you have one slightly bigger and very simple tax (which would still raise less than half as much as VAT, for example) which is a good tax; most households would pay much the same over a lifetime; and the impact on house prices would be negligible (might push them up a bit, might push them down).

Wednesday, 25 April 2018

Killer Arguments Against Citizen's Income, Not (13)

Chris Goulden at the Joseph Rowntree Foundation betrays his deliberate lack of understanding.

He lists the main pro's and then plucks some con's out of thin air:

A citizen’s income would require two big principles to be accepted and supported by the public, namely that:

1. Everyone should get a baseline level of state financial support, even if they choose not to do anything to try to earn money for themselves.

2. The basic marginal tax rate should be much higher than it is now, otherwise almost everybody’s net income from the state would rise, and there is no obvious way to finance this. (Some do not assume UBI must be paid for through income tax and suggest a wealth / carbon tax instead, or bigger cuts to state spending elsewhere, for example. None of these are easy options either).

Most politicians in the UK (or in England at least) are likely to regard both of the above as unacceptable to voters - a view supported by long-standing evidence on public attitudes to welfare.

3. A third objection relates to support for housing (and other) costs. For UBI to achieve its goal of removing the complexity and disincentives involved in means-testing, it would also need to replace support for housing costs. But with largely market-based rents, it would not be easy to include a simple rent element in a UBI payment without creating shortfalls for some or large surpluses for others. The same applies to means-tested childcare support. This counter-argument is strong – arguably public attitudes towards benefits and taxation could change but differing needs will not.

4. So, a central problem is that advocates of UBI either unconsciously or wilfully fail to acknowledge that the current system is designed to provide specific payments for people in specific circumstances (e.g. caring, disability, high housing costs, high childcare costs). If you sweep all of that away, you either have to level up, giving a massive boost to people without those specific needs (at huge cost), or you create a fall in income for those with them. Neither is remotely acceptable in any real world.

1. Agreed.

2. Is complete crap. The actual effective tax rate for claimants (i.e. about half the population, if you include Tax Credits) i.e. the total of PAYE deducted AND means tested benefit withdrawal is stupendously high and would fall considerably. There is no need to increase tax rates at all, and certainly not the basic rate of tax, that's basic maths.

As to "unacceptable" to voters, this is not an argument AGAINST simplifying and harmonising welfare and tax systems, it is an argument FOR educating voters. He is simply providing the brain dead with ammunition.

3. Housing related welfare can be kept running in parallel for the time being. Welfare for landowners is bad; means testing is bad, but needs must. Saying that "we have to means testing housing relating welfare, therefore we must also means-test non-housing related welfare" is just crap logic, you might as well go on to say we should means test non-cash benefits (state schools, NHS, the right to vote or use a public library etc).

He clearly knows bugger all about "means-tested childcare support". There's the superficially generous but savagely means tested Childcare element of Tax Credits (progressive) and the equal and opposite, weird and wonderful tax breaks for employer payments (regressive); as well as Free Early Education vouchers and kids who get a 'free' Kindergarten place at a state school (flat rate and non-means tested).

The actual cash amount/value that most parents get - regardless of which scheme(s) they benefit from - is pretty close to £90 per week per child, plus or minus £10. Ergo, we can get rid of all the overlapping crap and just give every parent of a pre-school age child £90 a week (a kind of age-related Citizen's Income) or a state school nursery place (and a small cash balance?) and there would be few winners or losers at either end of the income scale.

4. He then lists things which Citizen's Income proponents have always said should be left completely outside the system and continue to run in parallel. Disability payments should be transferred to the NHS budget anyway. . We dealt with housing and childcare costs above; he mentions them twice just to make his list appear longer. He clearly doesn't know about "caring" either. I assume he means "Carer's Allowance" which is just another reason for paying people a lower rate of Income Support by another name, so recipients thereof would be better off with a Citizen's Income (which would be pitched at the same £ amount as Income Support to start off with)

This whole Windrush generation fiasco - questions

Background here.

So some people grew up and lived here all their lives on the reasonable assumption that they were British citizens (for most things, being permanently resident here is good enough), even though technically they weren't.

What strikes me, is that only UK and Commonwealth citizens are entitled to vote at most elections (different for EU Parliament elections, which we won't need to worry about any more).

So, with the benefit of hindsight, either all their votes were invalid; they were de facto accepted as British citizens (in which case the matter is settled); or there is some leap of bureaucratic logic that says they were notionally citizens of their [parents'] country of origin (most likely a Commonwealth country), despite that country probably having no record of them?

I also wonder why this wasn't noticed decades ago, at the latest when they were old enough to need their own (British) passport to go abroad on holiday, which surely plenty of them must have done.

Hmm.

Tuesday, 24 April 2018

"An early warning sign to help spot struggling UK retailers"

I spotted the headline in City AM and thought, oh dear, this will just be some puff piece about getting the right product mix, and glosses over the fact that landlords aren't dropping the rent fast enough, but no, she nails it:

The metric we use to assess this aspect of a retail business is called ‘fixed charge cover’.

If you felt moved to calculate this yourself, it is a company’s ‘EBITDAR’ (earnings before interest, depreciation, amortisation and rent) divided by total debt service costs (net interest and rental expenses).

At its heart, however, this ratio illustrates the ability of a business to service its debt and rental obligations. Our rule of thumb is that when a fixed charge cover [drops to] 2x or 2.5x, serious alarms bells start to ring.

Take a look at the following chart, which ranks a dozen of the UK’s household-name retailers by their fixed charge cover and also shows the total returns on their share prices over the last six and 12 months.

As you can see, there is a huge correlation here. All the companies with a fixed charge cover of less than two times have seen their share price fall by a half or more over the last 12 (and the last six) months.

Monday, 23 April 2018

Killer Arguments Against LVT, Not (438)

I've not done one of these for a while as I hardly see any I haven't already done. There was a mildly original one from the comments at LibDem Voice last month.

He warms up with a couple of standard-fare KLNs...

William Fowler: Any tax not based on personal income or company revenue is going to be unfair, if you want to get at wealth an inheritance tax levy and sales tax on property/land/leases would surely do it.

Bollocks.

1. Land Value Tax is not about "getting at wealth", it is about, er, taxing land values. that's why it's called "land value tax" and not "wealth tax". The clue is in the name.

2. We already have IHT, CGT and SDLT, which are pretty much at the top of their own Laffer Curves, and between them, they capture less than one-tenth of the annual rental value of UK land - in a very cumbersome and economically damaging fashion.

Council tax makes up a small part of the council’s income and if you are going to replace government money with local taxes then does this mean a massive increase in taxes for the home owner or is all the burden going to be on companies with business rates replaced by LDV. Neither of which will have a very nice outcome.

Ah, the glorious double- if not treble-think.

Local councils are "government" just as much as the central government; both raise taxes and spend money. But miraculously, he does a diagonal comparison; comparing "government money" (good) with "local taxes" (bad) rather than acknowledging what most LVT supporters want - lower taxes on incomes ("government money") and higher taxes on land values ("local taxes"). So there would would be a massive reduction in the former to offset the "massive increase" in the latter.

And clearly, if you replace the worst taxes (list above) with LVT, home owners who are still working will see net large reductions in their tax bills. The same goes for the total taxes paid by businesses and their commercial landlords (how they share the spoils remains to be seen).

-----------------------------------------------------

... and then launches the Exocet of Home-Owner-Ism hypocrisy:

As Liberals, who believe in freedom of the individual, surely putting a huge burden on home owners, making them slave away at work forever or go on benefits to avoid it, would not produce much liberty?

As mentioned, working home-owners will be the group which would benefit most (insulated as they are from rent increases) if Council Tax, SDLT, VAT and NIC were replaced with LVT, that's just a mathematical fact. And clearly, for pensioners there would be a deferment option.

So presumably he is talking about the semi-retired people in fairly valuable homes who do not wish to contribute to society, neither by working nor by paying taxes.

So we could fire this back at him:

As Liberals, who believe in freedom of the individual, surely allowing the semi-retired in valuable homes to opt out of working and paying tax puts a huge burden on 'everybody else', making them slave away at work forever, as well as paying all the taxes to support the lifestyles of the self-same semi-retired, would not produce much liberty?

Thursday, 19 April 2018

Cattle news

From The Soaraway Sun:

IN THE MOOOOOOD Hilarious moment horny bull sneaks up behind female moped driver and tries to hump her

From the BBC:

Escaped cows herded into Darlington front garden

Car hits house - with a bad ending

From The Bristol Post:

A woman has died and residents have been evacuated after a car crashed into a house in Clevedon.

The woman who was killed was in the house and the occupants of the vehicle, a man and a woman, have been arrested and are currently in police custody.

The incident took place shortly before 8.30pm last night (Wednesday, April 18), on Yeolands Drive.

I've not tracked down the house on Google Maps yet, but I guess that like in most of these cases, the house is at the top of a T-junction or similar.

Top tips:

- don't buy a house at the top of a T-junction;

- if you own one, replace your front garden wall with concrete blocks;

- town planners and developers, please don't put houses at the top of T-junctions.

Wednesday, 18 April 2018

Stats confirm, don't build houses if you want to increase incomes.

In response to Ian Mulheirn's thorough de-bunking of the supply shortage narrative of the housing crisis, Capex has let John Myers, aka London YIMBY, have yet more publicity to rally the troops against the dissenting voices.

The article is just a re-heat of the same old tosh, however one thing that did catch my eye was this graph from the Resolution Foundation showing the relationship between rises in house prices and the increase in housing stock per capita. Myers comments "... the think tank’s report also contained the encouraging — and unsurprising — revelation that countries building plenty of homes have generally not seen huge price rises, despite low interest rates and a big banking sector."

Myers goes on "Accounting for changes in incomes would likely make the picture even clearer, as the government’s own numbers to justify the Housing Minister’s comments on immigration showed last week, because rising incomes greatly boost demand for bigger and better homes"

Leaving to one side that in Myers' articles, it's never location that is the biggest factor in the differences in prices across the UK, the point he raises is obvious. So for a bit of fun, let's correlate changes in incomes within countries during the same period(OECD data) with changes in housing stock:

What this shows is that an increase in housing stock per capita correlates with lower increases in incomes within countries at 0.61, which is probably about as strong as the scatter plot for price increases vs stock. It's interesting how Ireland is the outlier, probably due to their over supply on the run up to the crash.

On the face of it, it appears that if you want to enjoy bigger increases in incomes, the last thing you want to be doing is build loads of housing.

Of course, this is wrong. But my point is, without putting things into their proper context, all sorts of misleading conclusions can be drawn. I'm afraid that's why the current policy of blaming planning and under supply for housing issues is wrong. It's being pushed by those with a very narrow field of vision.

For the record, I think a land value tax would result in a huge amount of redevelopment. Only it would then be property facilitated and directed by planners with the right incentives i.e. to maximise aggregated land rents. Instead, in large part due to the supply side fanatics, we'll yet again end up with the worst of both worlds i.e. more crap and not much/no improvement in affordability.

Tuesday, 17 April 2018

Most employees pay far more National Insurance than Income Tax

The 'earnings threshold' for NIC is lower than the personal allowance for income tax; and for basic rate taxpayers, total NIC is 25.8% of earnings above the threshold but income tax is only 20% of earnings above the personal allowance.

At the top of the basic rate band, it's £9,786 NIC and £6,900 income tax.

Above that, it flips over, NIC is 'only' 15.8% of earnings but income tax is 40%.

The break-even point at which you pay the same amount of NIC as you do income tax is about £58,300, which you can check here, so only the top few per cent of employees actually pay more income tax than they do NIC.

VAT raises approx. the same amount as National Insurance, meaning that a majority of employees probably pay more in VAT than they do in income tax as well.

Just sayin'.

Monday, 16 April 2018

Sunday, 15 April 2018

Economic Myths - imposing a minimum wage will always lead to falls in employment and output

Opponents (broadly, "right wingers") say that wage levels are set in a competitive market, so if the minimum wage is higher than this, this will cost jobs and reduce output. Defenders of minimum wages (broadly, "left wingers") say that it levels the playing field between exploitative employers and exploited workers and insist that any small fall in employment is a price worth paying.

Each side puts out their studies which purport to prove their theory. I'm not really convinced by either set of 'facts' as people are highly selective and tend to find what they are looking for.

(I personally am heartily indifferent about the National Minimum Wage, my view being that the best guarantee of workers' rights is a growing economy and full employment - i.e. get rid of VAT and supertaxes on employment income such as National Insurance Contributions. We can back this up with a Citizen's Income, which strengthens the bargaining position of potential workers slightly, especially when it comes to low-wage jobs.)

I have recently stumbled across a theory that says, evidence shows that the negative impact on employment and output was not only nowhere as bad as the doom-sayers predicted, but that in some situations, imposing a minimum wage can actually increase employment and output.

Sounds very counter-intuitive, but actually it makes sense. This is because most businesses have some monopoly/monopsony power (they are two sides of the same coin).

Let's start at the very beginning with a business in a perfectly competitive market where labour is the only variable cost with a given supply curve and a given demand curve. The level of output of the business in question would be 9 units, wages £10.40 and selling price £11, being the highest level of output before the business tips into losses:

The columns for marginal cost and revenue are the total cost/revenue at that level of output, minus the total cost/revenue if one unit less were produced and sold. The relevance of this will be explained further down.

(I am perfectly aware that no business knows exactly what its marginal costs per unit are, let alone what its marginal revenue per unit it, and that most businesses do some sales at a loss, whether by accident (budget overrun or customer doesn't pay) or by design (loss leaders). Nonetheless, businesses must have some collective intuitive grasp of this or they'd all be bankrupt. 'Home builders' are the crassest example of this, in the short term, more supply depresses prices and costs would increase rapidly).

So if a minimum wage of £12 is imposed, the business in a perfectly competitive market has to reduce output to 8 units, wages £12 and selling price £13, being the highest level of output before the business tips into losses. This is bad, and what the opponents predict:

As we well know, most businesses have some monopoly power (can restrict supply) and, especially if there is permanent un- or under-employment, a stronger bargaining position than potential employees, which we shall consider monopsony power for the purposes of this debate.

Such businesses (or industries) do not end up setting prices at just above costs, which is the optimum position for the economy as a whole. They choose the level of output which maximises profits, and you can't fault them for that. Some interpret this to mean that businesses (should) set output at the level at which any further increase in output means that marginal costs would exceed marginal revenue.

So this business restricts output and employment to 5 units sold for £16 each, total profits £44, wages of £7.20 per hour. There's no point going to 6 units - marginal costs £12 exceed marginal revenue £10 and profits would fall.

What happens if the minimum wage is set at £8 per hour? While average wages go up, the marginal cost goes down to a flat £8 for the first six units of labour. The new profit-maximising level of output is now 6 units sold for £15 each, total profits £42, wages of £8 per hour.

Higher wages, more jobs, more output, lower prices and monopoly profits (rent) shaved back a bit. What's not to like?

Yes, I know this is all hypothetical, but there are simply too many studies showing that there is no measurable negative impact of minimum wages on employment levels to simply be dismissed out of hand, however biased the authors. So I think that there is something in it, however difficult it is to explain.

Or maybe both sides (left wingers and right ringers) are half-right and the extra jobs in monopoly businesses cancel out (or outweigh) job losses in competitive businesses. This would still be a good thing, if those competitive businesses are only competitive because wages are depressed.

Friday, 13 April 2018

In reply to Bayard's question about why people spend so much on housing.

From here

Me: If your point was that land prices are the inverse of interest rates and/or proportional to credit availability, you are clearly correct.

Bayard: Yes, but why? Why do so many of us spend more on land when we have more to spend? We don't tend to spend more on food, cars or holidays in quite the same way. Most people walk into a car showroom with an idea of which car they would like to buy and try and buy it for the least they can. The same people walk into an estate agent's with an idea of how much they have to spend and try and get the best house they can for that money. That's the quirk.

It has something to do with marginal utility.

For most people on OK incomes, mass produced stuff like cars, food, holidays, are all relatively cheap. Everybody has their own preferences about how to split their money between cars, food, holidays.

Let's take cars, some people want to have the shiniest, newest model, whatever it costs, but most are are happy to buy second hand (most cars are bought and sold several times, so most car purchases are second-hand). Those people get less enjoyment from buying a car that costs £1,000 more than they would from spending that £1,000 on something else.

That car is their "ideal" car, and for most people is easily affordable. For me, the "ideal" car costs about £2,000, anything more than that is money down the drain (repairs, on the other hand...). Even if I earned three times as much, the £2,000 car would still be my "ideal" car. (Knowing me, I'd just buy more £2,000 cars. MGF is next on the list).

Housing on the other hand is incredibly expensive, bearing in mind how long ago the bricks were piled up and how little ingenuity it took to do so.

Each household's "ideal" home is the home where the extra enjoyment from buying one that costs £10,000 more would be less than the extra enjoyment from spending £10,000 on something else. And for most people, this "ideal" home is way out of reach, financially, they simply don't have the extra £10,000.

So our only choice is to pare back 'other spending' and set our housing budget as all income not needed for 'other spending' - and then spend all of that housing budget on getting the nicest we can afford within that budget.

----------------------

There's also the point that people assume house prices will go up and up, so they don't really view it as a cost, they see housing as an "investment" which generates capital gains and income (which it does, or at least, it saves paying rent). On that basis, spending every last penny on housing makes sense from an individual's point of view.

From the point of view of society as a whole, it is madness because we are all trying to outbid each other and so the monopolist (the land owner) is the only winner. If an entire generation of tenants and first time buyers formed a cartel and agreed that none of them would spend more than 10% of their income on rent or mortgage repayments, then they'd all end up in the same homes as they would have done but at one-third of the current cost.

Wednesday, 11 April 2018

Method or Madness?

I, like most people, assume that Donald Trump is just an overgrown spoilt brat child who has no concept of his actions having negative consequences, it's all just "I want, I want, I want".

When he threatened North Korea with "fire and fury" or started the tit-for-tat tariff game with PR China, I, like most people, thought, Oh fuck, where will this end?

But possibly, he is a tactical genius, was just bluffing and planned this all along, headlines from the last few days:

North and South Korean leaders to meet for historic summit on April 27

Secret, direct talks underway between US and North Korea

China's President Xi promises to CUT car import tariffs as he buckles in trade war with Trump and warns against ‘Cold War’ mentality

Or possibly, he won't realise what a dangerous/stupid game he is playing and this will just spur him on to make ever more outrageous demands. Like threatening to nuke London if he doesn't get an invitation to that wedding thingy to which - if the MSM is to be believed - everybody wants an invitation?

Home ownership doesn't make you happy

I recently read that Finland had been ranked the happiest country in the world by the UN's Sustainable Development Solutions Network, which got me looking into its housing. After all, it has long been a tenet of this blog that home-ownership is a Good Thing, so perhaps the Finns were big on that.

Wikipedia gives a list of countries ranked by rates of home ownership and Finland, at 30th place with 72.7% is not hugely different from the UK at 42nd place with 64.5%. Indeed, of the top twenty countries by home-ownership rate, only six appear in the list of the top fifty happiest countries, with only Norway with 82.8% and the second happiest and Singapore with 90.8% the thirty-fourth happiest, having more than 80% home-ownership. Meanwhile Switzerland, the fifth happiest country, just scrapes in at the bottom with 43.5% home-ownership.

Finnish housing policy comes in for some plaudits but closer examination shows that it is not markedly different from the UK's. OK, they have a better attitude towards social housing, but they are still big on second homes (A Finnish saying is "Happiness is having your own red summer cottage and a potato field"), so housing wise, we do not have far to go if we are going to be more like the happiest country in the world. Just don't count on it making us any happier if we get there, though.

Monday, 9 April 2018

Poacher turned Gamekeeper

Ed Conway in 2009, rooting for LVT:

Second, the Government must reshape the tax system so that it does not favour home ownership. This may mean experimenting with a land tax, whereby families pay annual taxes based on the value of their home and land; it may mean imposing capital gains tax on first homes. Both steps would help prevent another bubble, although they would have unpredictable side effects.

Ed Conway in 2018:

It’s not just left-wing economists proposing new taxes on wealth and property these days, says Ed Conway. Last month the Resolution Foundation, chaired by the former Conservative minister David Willetts, proposed replacing council tax with a new property tax of 1%-2% of the home’s value.

But the proposal is flawed. For a start, it would be fairer to charge a percentage of the un-mortgaged portion of the property. That, however, would send solvent homeowners scuttling to take out new mortgages.

Most importantly, how does one determine value fairly? Visual valuations would benefit the banker who has dug out a three-storey basement. As for using sale prices, some don’t appear on the Land Registry. And what about the old lady who’s lived in her home since it was a slum and can’t afford the bill?

In any case, while we may not have a formal wealth tax, the British “collect proportionally more wealth-related taxes than anyone else”. Inequality is average compared to the rest of Europe and our top earners already pay a “near-record proportion of the tax base”. So by all means modernise council tax, but the government should steer clear of new property taxes. They are “fiscal dynamite”.

"Fiscal dynamite", eh? He's not wrong there, but otherwise a rich seam of KLNs and full marks for including that mythical beast, the PWIM.

Killer Arguments for LVT, Not (2)

Following on from my previous post, the same factors that mean that a 100% LVT replacement tax won't cause a wiping out of the landlord class, mean that LVT won't make house prices "affordable", where "affordable" doesn't mean "prices that people can afford" (using that definition of "affordable", the only unaffordable house is an empty house) but "prices at a level they were in the 1980s" or at least "a smaller chunk of my monthly outgoings than at present".

As can be seen from this graph, house prices are pretty well inversely proportional to interest rates, i.e. they are proportional to what people can afford to borrow:

However, if LVT is a replacement tax and, given no change in interest rates, then, by and large, the average would-be homeowner is going to be no worse off than they were before. The extra they have to pay in LVT will be balanced by the amount they are saving on income tax and VAT, so the amount they can afford to spend on a mortgage every month will be roughly the same as it was and thus the average house price will remain pretty well unchanged. Indeed, the improvements to the economy caused by the removal of deadweight taxes is likely to put house prices up, by making the housebuying public better off.

Sure, Londoners and Roselanders will see prices fall and inhabitants of places like Neath will see them rise, but these falls and rises will be caused by falls and rises in what these people can afford to spend on mortgages, so true affordability will remain unchanged.

What has made houses unaffordable in the past twenty years is not so much the price, because the price of land is linked to what people can afford to pay and therefore is a system with negative feedback, but the requirement for ever bigger deposits, which has no link to anything apart from government policy.

Daily Mail on top form

High-flying lawyer who rents out £320,000 house* where two men died in suspected carbon monoxide leak is being investigated by police

* Or not as the case may be - going by Zoopla, that does seem a very low price for a three bed semi in Edgware.

"Restaurant diner cheesed off by Asda baked camembert"

From The Times:

A diner who ordered a £13 baked camembert at a restaurant was served one costing £1.15 from Asda which was still in its round supermarket box. Emma Daniels chose the sharing starter at Severnshed to eat with her partner.

It arrived on a board with bread, chutney and the cooked cheese sitting upside down inside the Asda wrapping. She went on the TripAdvisor website on Saturday and left a two-star review for the Bristol restaurant.

OK, it was a bit naff to leave it in the supermarket box, rather than prising it into a "terracotta dish", but apart from that, so what? Don't people know that when you eat in a fancy restaurant, the retail price of the food you eat is only 10% - 20% of the final price of the meal incl. VAT and tip?

Either it tasted nice or it didn't, end of. The £13 price is meaningless, they chose to pay that much.

Unless this is all a clever ASDA marketing campaign..?

Friday, 6 April 2018

In the interest of balance...

Bayard posted here in response to something Simon McKenna had posted on Facebook. Simon McKenna responded on Facebook:

"... I must say the fact that Mark fails to understand my assertion that fiscal economics aside, private rent extraction is morally wrong, quite disturbing (although it is quite common!). Just add that I totally agree that everyone will benefit from 100% LVT. That was not the point I was making, so your presentation of your rebuttal is misleading. I am not advocating "class war" by reminding people that the privatisation of land is wrong:

A) We have to understand that economics is inherently ethical. Poverty isn't a merely fiscal (therefore acceptable) side effect of an economic system that need not cause poverty. Poverty is a moral evil. Ask anyone who suffers from it, or go observe some. Even if you just think about it, most poverty is unjust. It isn't caused by the poor because they fail to work, it is caused by the system which heaps benefits on unearned wealth and penalises work.

B) As a member of a political party, you should understand that politics is about morality as much as economics is about morality. Take the recent arguments advanced by the Conservatives that "Britain must pay it's debts". This is an erroneous argument economically, which relies on an incorrect moral analogue to the household budget. It ignores the fact that countries have to be in debt because that is how money is created. https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

However, people supported it because the moral force of the argument compliments economic illiteracy - one must pay one's debts, therefore we must pay our debts. Likewise, people support notions of a "deregulated free market" because they think people should be free to trade (even though all markets are created and restricted by rules), people still support Marxism because they think it is wrong that one class should rule another (despite the evidence of the terrible economic and moral consequences of Marxism). All of these arguments are factually problematic but have been unbelievably successful because have enormous ethical appeal. Consider Churchill's speeches in support of LVT - he makes the moral argument - it is wrong that one should profit despite not working. It is not class war, it is simple morality.

My original point was to remind people that the private collection of rent is not only extremely economically counterproductive for everyone, it is morally wrong, since no one created the land on which we must all dwell, no one can claim to have the right to the product thereby generated."

Let's talk about anti-Semitism in the Labour Party without addressing anti-Semitism in the Labour Party

There's a glorious amount of hand wringing at The Guardian and the like, but it's all meaningless waffle.

To my mind, anti-Semitic (which is an inaccurate way of saying "anti-Jewish", seeing as semitic means people from a certain part of the Middle East; and most Jewish people aren't, they don't even look as if they are, unlike, say, Greeks) people are in a few quite distinct categories.

1. Straight forward, BNP-style racists. I suppose there is a minority of (white) people in Labour who are just racist. I think society can handle this, we just ignore it, there has always been a 5% or so minority prepared to vote NF or BNP (or hijack UKIP when it was still worth hijacking), they'll never go away, but the UK is still one of the least racist countries. By and large, they have no influence and do not carry out random attacks on Jewish people or synagogues, so forget it.

2. The weird "Jewish people are lizards who run the world" fuckwittery and Holocaust denial (David Icke and David Irving), this is an even tinier minority or conspiracy theory nutters, who are pretty harmless.

3. The trendy "Israel is evil and we must stand up for our Palestinian brethren" lefties, who are not really anti-Semitic at all. It's just a phase that people go through, like having a Che Guevara poster. I think that most of these trendy lefties are bright enough to realise that 'the country Israel' and 'Jewish people' are entirely separate and independent, and most Jewish people are heartily indifferent about Israel, in the same way as English people have no strong opinion either way on Australia.

Clearly, by Western standards, the Israeli government has been and continues to pretty nasty in many respects, but by Middle East standards it's a shining beacon of liberty and democracy, so again, not an issue.

4. UPDATE: There is a category which also overlaps with 1, 2 and 3, which is what Lola addresses in the comments. Banks are pretty evil and for some reason, people stereotype bankers as predominantly Jewish and vice versa, which is a) bollocks and b) banks are just piggy backing on Home-Owner-Ism and rent seeking generally, the far greater evil. Some lefties are even dafter and equate banking (largely bad) with capitalism (largely good) which is a bloody shame, from a capitalist's point of view.

5. Then of course, the ones we can't mention. From what little info we have, most of the really rabid anti-Semites in Labour/Momentum are in this category. Can you guess what it is yet? I did mention it once on Twitter and was roundly derided as a racist, so I don't know why I bother. And as long as you're not allowed to mention it, you can't fix it. We know for a fact that unlike the BNP-style racists, these people do actually carry out attacks against Jewish people, synagogues, shops etc (thankfully in the UK a lot less than in France or Sweden).

Thursday, 5 April 2018

"We don’t know why deadly crime is rising in London, says government that cut 20,000 police"

Newsthump hits the nail on the head.

Wednesday, 4 April 2018

"Over-50s hold 75 per cent of UK housing wealth"

From City AM:

Homeowners over 50 hold three-quarters of the country’s housing wealth, according to new research from global property adviser Savills. These older homeowners, who have benefited from years of strong housing price growth, now own 75 per cent of all equity, with a total value of £2.8 trillion.

Not sure why they have such a low figure for equity, Savills reckon that the total value of all UK housing is £6.8 trillion and 75% of that is £5.1 trillion. This suggests total mortgages held by over-50s is £2.3 trillion.

Seeing as most over-50s will have bought over twenty years ago when houses were easily affordable, the original cost would have been (say) one-third of £5.1 trillion minus 10% deposit = £1.5 trillion, and in turn, just about all of this should have been paid off by now. So the £2.8 trillion is all second mortgages and buy-to-let mortgages.

Be that as it may, most of that £5.1 trillion is an unearned freebie whether people have remortgaged or not.

Tuesday, 3 April 2018

Health tourism and acceptable losses

From fullfact.org:

Who is a “health tourist”?

Qualifying for free NHS care isn’t based on nationality or where someone was born. It’s based on whether you are “ordinarily resident” in the UK and the type of treatment you need... The government has estimated that treating deliberate health tourists and those taking advantage costs around £100 to £300 million a year. Those are incredibly rough figures.

At the moment there are some services which, no matter whether you are “ordinarily resident” or not, you can’t be charged for. The costs estimated by the government also include these services, like going to see a GP or using Accident and Emergency. So even if the NHS charged for all the services it possibly could and received the money, it wouldn’t cover the full amount health tourism is estimated to cost.

From NHS Digital:

Hospital admissions in England rose to record levels last year, with 16.2 million admissions during 2015-16 - up from 12.7 million ten years ago.

OK, so let's assume the NHS starts doing identity checks on every single hospital patient to deter health tourists. Firstly, it will lead to some unpleasant situations where somebody is a bit old and doddery and simply can't produce a passport or driving licence etc, what are they going to do, turn them away? I doubt it. Leave them in the waiting area while a relative is despatched to try and rustle something up?

I can easily imagine that this will add £20 to the cost of a hospital visit. Some officious person will disappear with your passport and council tax bill for ten minutes just to check they are legit (i.e. have a nice cup of tea while you're waiting).

Cost of weeding out health tourists = 16.2 million x £20 = £324 million

Upper end of estimates of cost of health tourism = £300 million.

So, as unpalatable as this may sound, it's cheaper just to accept it.

Monday, 2 April 2018

"The strange phenomenon of twin films" - an excellent list of short lists

Steve McIntosh at the BBC has done an excellent list of my favourite kind of list, one with two things on it.

Films about a comet/asteroid hurtling towards Earth at an alarming rate, threatening the existence of the human race released between May and July 1998?

Films about the eruption of a volcano threatening the life of locals released between February and April 1997?

And so on.

Sunday, 1 April 2018

Killer Arguments FOR LVT, Not

On a post on the Facebook LVT group, one Simon McKenna made the following comment:

"..the private collection of rent is not only economically imprudent because it periodically destroys the economy, it is wrong!"

Leaving aside the periodic destruction of the economy, I don't think that it is a valid argument for LVT that it will be an instrument of social justice. This idea has quite some traction, especially amongst the ranks of the class warriors and ties into the populist landlord-bashing cause of enduring appeal.

However, there are flaws:

1. Ricardo's Law of Rent indicates that the raising of tenants' incomes caused by the lifting of other taxes on economic activity will enable landlords to raise rents to compensate for the LVT they have to pay, also, as mentioned in previous posts, the increase in economic activity caused by the removal of these taxes will have a similar effect. Although rents will be stripped of their location value, given 100% LVT, the non-location value part of the rent will increase, across the board.

2. This means that, although in places where location value is very high, e.g. in London, the fall in rent receipts will be such a high percentage that it couldn't possibly be matched by a rise in income, given current levels of overall taxation, in areas of very low location value, e.g. Neath, then the fall in rent receipts due to LVT would be almost zero, whereas almost everyone would be saving at least 20% VAT, even if they have no income worth taxing, so landlords would be better off.

3. Since farmland has been deprived of all location value by the Town and Country Planning Acts, it will not be taxed and so farm rents will be unaffected.

So, numerically, the majority of landlords would benefit from a transition to 100% LVT as the sole form of taxation, including some of the richest and most aristocratic. That doesn't look like much of a victory in the class war.

{kind=link}